Key Takeaways:

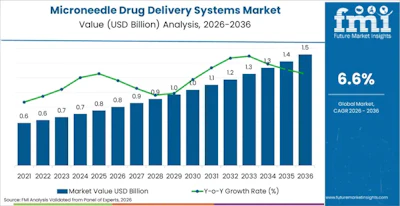

- The global market for microneedle drug delivery systems is projected to grow from $0.8 billion in 2026 to $1.6 billion by 2036, driven by demand for painless alternatives to traditional injections.

- Key business challenges include overcoming manufacturing scalability constraints, ensuring consistent dosing accuracy across patient populations, and navigating complex regulatory environments for drug-device combinations.

- Competitive advantage is increasingly tied to strategic partnerships, investment in proprietary micro-fabrication technologies, and the ability to integrate therapeutics with advanced delivery platforms.

Growing pressure on healthcare systems to improve operational efficiency and the post-pandemic acceleration of decentralized care are creating significant opportunities for new drug delivery technologies. Microneedle systems, which enable minimally invasive and self-administered therapies, are emerging as a key solution to reduce nursing workloads, minimize needle-stick injuries, and lessen dependency on cold-chain logistics for vaccines and biologics.

A new report from Future Market Insights (FMI) projects the global microneedle drug delivery systems market will expand at a 6.6% compound annual growth rate, reaching $1.6 billion by 2036 from an estimated $0.8 billion in 2026. The technology's ability to provide pain-free administration for a growing pipeline of biologics and vaccines is a primary driver of this growth.

From Niche Innovation to Mainstream Infrastructure

The market is moving beyond specialized applications and becoming a more integral part of healthcare delivery. "The microneedle drug delivery systems market is transitioning from niche transdermal innovation into a mainstream healthcare infrastructure solution," said Sabyasachi Ghosh, Principal Consultant at FMI. He noted that "companies capable of combining scalable manufacturing, regulatory compliance, and advanced drug-device integration will gain long-term competitive advantage across pharmaceutical and clinical channels."

According to the report, solid microneedles are expected to lead the product category, accounting for a 52.6% market share in 2026 due to their manufacturing simplicity and mechanical reliability. Hospitals remain the dominant end-use segment with a 44.1% share, supported by large-scale vaccination programs and institutional procurement needs. North America is forecasted to lead the market geographically, holding a 31.7% share.

Navigating Commercialization Roadblocks

Despite the strong market forecast, significant operational and regulatory hurdles stand in the way of widespread adoption. According to FMI, companies must address complex regulatory approval pathways for novel drug-device combinations. Furthermore, manufacturing scalability remains a primary constraint, alongside the technical challenge of ensuring consistent and accurate dosing across diverse patient demographics.

The competitive landscape is being shaped by these challenges. Key players such as 3M Company, Becton, Dickinson and Company, and Vaxxas Pty Ltd. are focusing on strategic partnerships and acquisitions to bolster their capabilities. Investment in proprietary micro-fabrication technologies and a focus on improving manufacturing scalability are central to current competitive strategies as companies work to meet the rising demand from both healthcare providers and patients.