The global market for pharmaceutical inspection machines is projected to grow to $1.62 billion by 2031 from about $1.14 billion in 2026, a 7.2% compound annual growth rate, according to a June 11 forecast from research firm MarketsandMarkets.

The report links demand to rising manufacturing volumes across generics, vaccines, biologics, and specialty drugs, which are pressuring quality-control operations to automate inspection of vials, syringes, ampoules, cartridges, and packaging. Automated systems—often combining machine vision, AI-powered analytics, X-ray, checkweighers, sensors, and robotics—are being deployed to detect defects, contamination, fill-level issues, and packaging errors at line speeds that outpace manual inspection.

Key takeaways for industry:

- Where the spend is: Hardware-centric inspection systems account for the largest component share, outpacing standalone software as manufacturers prioritize end-to-end automated quality checks, the firm said.

- Who’s buying: Pharmaceutical manufacturers represent the largest end-user segment, reflecting high-volume operations, tighter regulatory expectations, and ongoing investments in smart manufacturing and process automation.

- Regional outlook: Asia Pacific is expected to post the fastest growth, driven by capacity expansion in China, India, Japan, and South Korea; increased output in generics, biologics, and vaccines; and broader adoption of Industry 4.0 technologies amid stricter quality oversight.

Business impact:

- CAPEX timing: With a multiyear growth runway through 2031, procurement teams should align inspection investments with planned scale-ups in injectables and biologics, where container integrity and particulate control are under tight scrutiny.

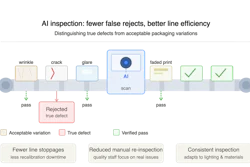

- Throughput vs. false rejects: As lines accelerate, specifications should balance inspection speed, sensitivity, and acceptable false-reject rates to avoid downstream bottlenecks and waste.

- Validation and data integrity: Buyers should evaluate GAMP 5 and 21 CFR Part 11 readiness, audit trails, and model governance for AI-enabled vision systems to meet FDA, EMA, and PIC/S expectations.

- Integration: Selecting platforms that integrate with MES, QMS, serialization/track-and-trace, and plant data historians can streamline investigations and continuous improvement.

- Retrofits vs. greenfield: Brownfield upgrades (vision retrofits, modular X-ray) can deliver near-term OEE gains, while greenfield builds may justify fully integrated robotic inspection cells.

- Service footprint: In Asia Pacific, local service, spare parts availability, and training coverage will be pivotal as sites scale and diversify product formats.

By the numbers:

- Market size: $1.14 billion (2026) to $1.62 billion (2031)

- CAGR: 7.2%

- Largest component: Inspection systems (hardware-centric)

- Largest end user: Pharmaceutical manufacturers

- Fastest-growing region: Asia Pacific

What to watch:

- Expansion of AI/ML in defect detection and the regulatory posture on validation of adaptive algorithms.

- Increased inspection complexity for prefilled syringes, cartridges, and complex biologic presentations.

- M&A and partnerships among equipment makers, machine-vision providers, and robotics firms to deliver turnkey solutions.

- Evolving regional standards that may influence equipment specifications and qualification timelines in APAC.